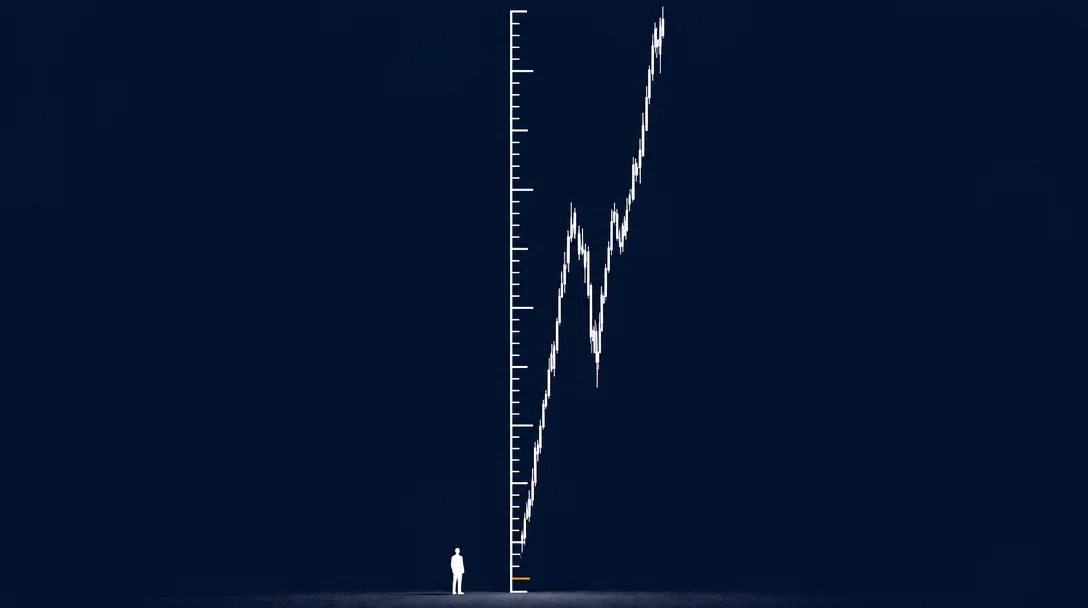

Scale comparison: one trading day vs. one career

A 1% S&P 500 intraday swing vs. median lifetime earnings

Wage income isn't just small — it's structurally incompatible with the financial risks most people take on. A first-principles argument for why the standard playbook of salary → mortgage → equities is leverage exposure in disguise.

Add more perspectives or context around this Drop.